Phosphate: The Commodity That Feeds Half the World Is On the Brink

Phosphorus cannot be synthesised. Full stop. Unlike nitrogen derived from natural gas, phosphate has to come out of the ground. No phosphate, no fertiliser basket. No fertiliser, no food for roughly four billion people.

So when the three largest supply sources all hit structural trouble at the same time, it is worth paying attention.

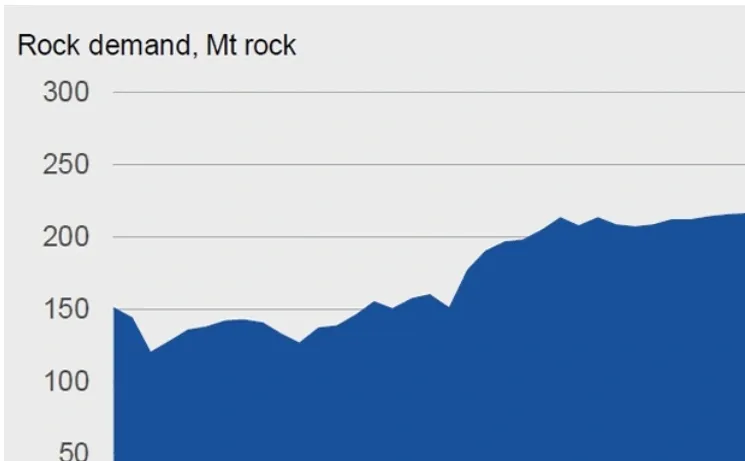

The Supply Picture Is Worse Than You Think

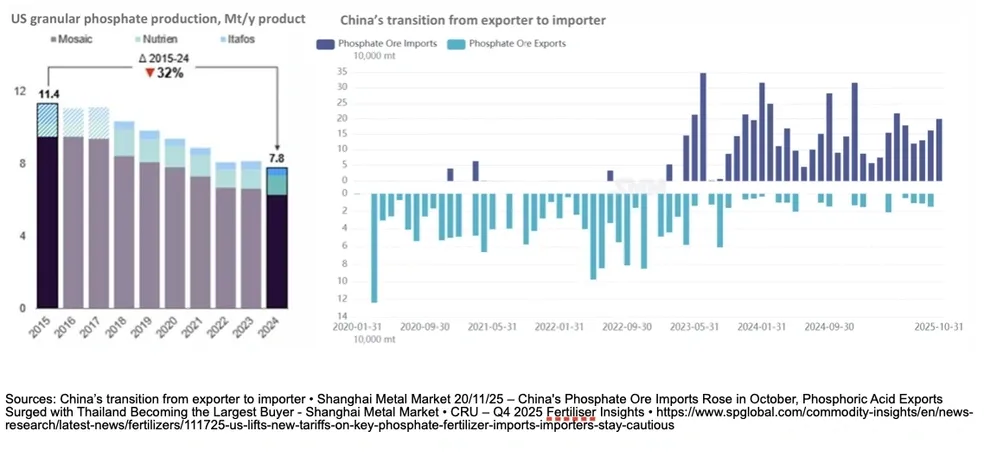

In late 2025, China’s NDRC directed a suspension of major phosphate fertiliser exports, formalised through industry-level directives rather than a single public order. By March 2026, the restrictions were firmly in place across most phosphate categories. This was not a surprise to anyone watching. Beijing has been tightening the screws since 2021, prioritising domestic consumption as its mines deplete and LFP battery demand eats into supply. China became a net importer of phosphate rock in 2023 and imported roughly 2.9 million tonnes in 2024. Downstream, it still exports processed fertiliser but the direction is clear for now, domestic demand is cannibalising supply that once fed global markets.

The US has seen phosphate production fall nearly 50% over 25 years. The USGS added phosphate to its Critical Minerals list in November 2025. There is still significant downstream processing capacity in the US, but the feedstock is disappearing. Fertiliser costs comprise 40% of the direct cost of corn. Bipartisan support for phosphate supply chain security is not a hard sell.

Russia, roughly 10-12% of global phosphate fertiliser trade, has been problematic since Ukraine. That has not changed.

Then the Strait of Hormuz. The Iran conflict has choked fertiliser exports from the Gulf. Five countries reliant on that strait accounted for 23% of global ammonia trade, 34% of urea trade, and 18% of MAP and DAP trade in 2024. Josh Linville from StoneX provided a good summary recently: if nitrogen markets are bad, phosphate is worse.

This is the kind of analysis we publish daily in The Drill Down. Subscribe HERE for free.

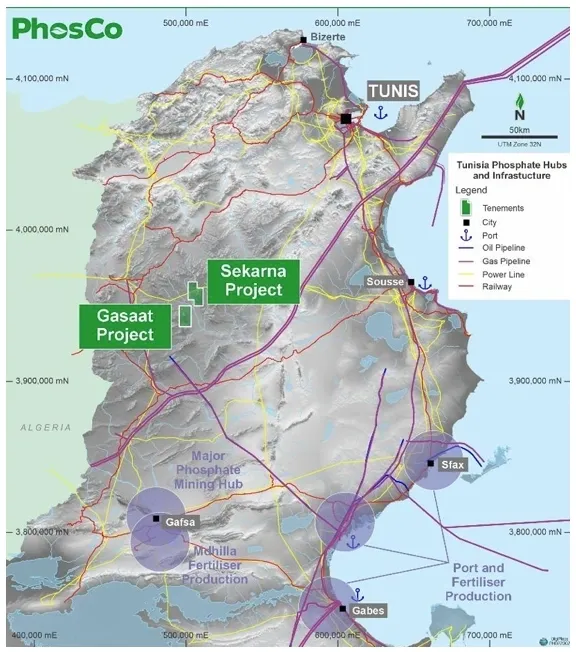

PhosCo and the Tunisian Reframe

PhosCo Ltd (ASX: PHO) owns 100% of the Gasaat Phosphate Project in Tunisia. A 112 square kilometre exploration permit, roughly 210 kilometres southwest of Tunis, discovered by the company in 2010.

Tunisia is geographically blessed, being the northern most country in Africa, and better understood by most European investors and tourists than Aussies due to its proximity. The country is closer to Sicily than it is to the Middle East and consistently ranks as a top destination for European tourists leaving Europe. The EU treats it as one of its most established Mediterranean trading partners. Tunisia’s abundant sunshine isn’t just a drawcard for tourists, it’s being harnessed to attract major renewable energy investment from players like Scatec and AMEA Power. That same ambition is now being directed toward the country’s mineral resources sector.

Strong support for development.

The Tunisian government has signed an MOU supporting Gasaat’s development, and the project has proactive local support with communities to benefit from 10% project participation.

Gasaat sits on the Mediterranean. Product can ship through Suez, through Gibraltar, or straight across to Europe. Logistics optionality that most African phosphate projects simply do not have. When the alternative sources are China (banned exports), the US (depleting), and Russia (sanctioned), that matters.

Strip Ratio: One Number That Changes Everything

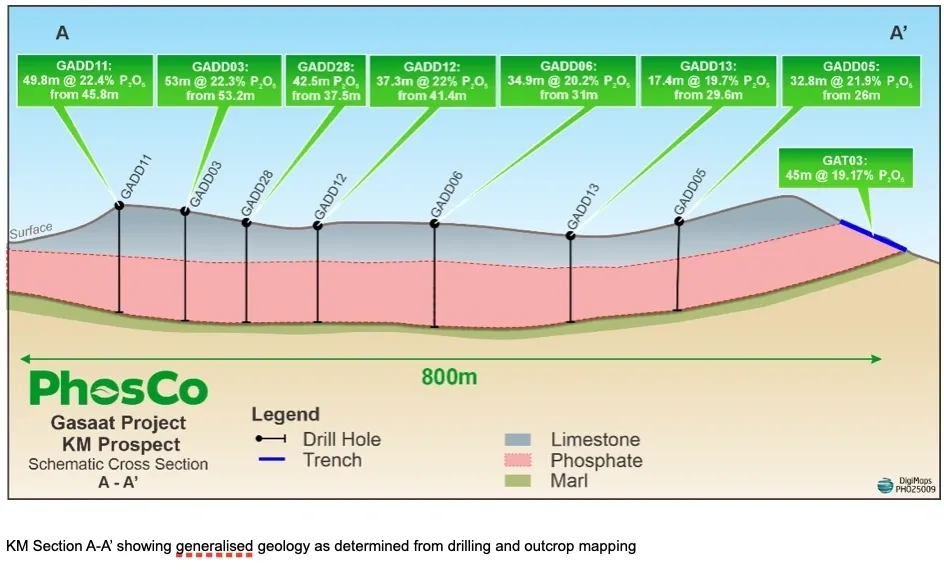

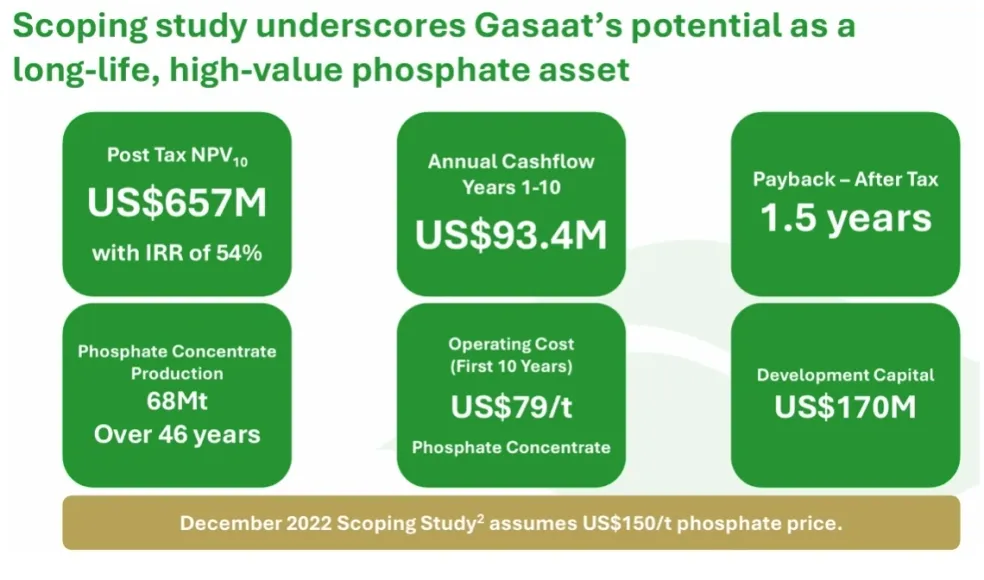

Gasaat hosts a JORC 2012 Mineral Resource of 146.4 million tonnes at 20.6% P₂O₅, defined from drilling at just two of nine prospects. At 1.5 million tonnes per annum of concentrate, that is close to a 50-year mine life. The December 2022 Scoping Study produced a post-tax NPV₁₀ of US$657 million, IRR of 54%, and payback of 1.5 years at a US$150 per tonne phosphate price that now looks conservative.

The 2022 study assumed a 3.5:1 strip ratio from the KEL deposit. Since then, PhosCo has drilled the KM prospect which is right next to the planned processing plant at a strip ratio of 1:1. SAB, in the centre of the permit, sits around 2:1. Going from three and a half buckets of waste per bucket of pay dirt to one bucket changes the cost base dramatically. Any investor can do that arithmetic.

KM drilling has delivered thick, high-grade intercepts: 53 metres at 22.3% P₂O₅, 49.8 metres at 22.4%, 42.5 metres of phosphate from 37.5 metres depth in the latest campaign. The geology is simple. Broad, thick seams.

In March 2026, drilling at the DOH prospect confirmed a new discovery, a phosphate horizon averaging 13 metres thick across 1,300 metres of strike and over 600 metres of width. That is another front entirely, and it has not been priced in.

Met test work is underway with flotation results which will feed into the updated scoping study.

The EBRD Grant: Actual Money

I spend a lot of time in the critical minerals space. There is no shortage of announcements, MOUs, policy frameworks, and task forces. Most of it is theatre. Very little puts capital in the ground.

PhosCo has something different. The European Bank for Reconstruction and Development which is a multilateral bank backed by over 70 member countries, with over €200 billion deployed globally gave PhosCo a €1 million grant. Cash. Not equity. Not debt. Not a conditional letter.

When the EBRD backed Adriatic Metals in Bosnia, they took an equity stake, paid £6.2 million for 2.6% of the company. With PhosCo, they led with a grant, because they consider phosphate supply diversification strategically important for food security. The equity component comes later. They clearly view Gasaat as a project with the potential to deliver meaningful impact, both for the sector and for the country. Post the updated scoping study, the EBRD has 120 days to exercise its option by investing A$7.5 million to become a PhosCo shareholder. Grant first, investment second. I have not seen EBRD structure a mining deal like that before.

If exercised, those funds cover a significant portion of the Bankable Feasibility Study.

The EBRD is a big supporter of Tunisia, backing a range of initiatives, including a €160 million contribution to the country’s rail modernisation program. The African Development Bank has approved funding of US$110 million to support the environmental modernisation of Tunisian Chemical Group. The Saudi Fund for Development has financed a US$55 million loan specifically for phosphate railway renewal in the Sfax-Gafsa-Gabès corridor. The IFC, EIB and the World Bank are also active in country. When that much multilateral capital flows into a jurisdiction, the country risk conversation shifts.

What Comes Next

Maiden resource estimates for KM and SAB are expected in April. Mine planning follows. The updated scoping study is guided for Q2, incorporating the strip ratio improvements, infrastructure optionality, and met test work results. BFS commencement kicks off thereafter.

The company raised $5 million in an institutional placement in February 2026 at $0.12 per share, giving it a pro forma cash balance of $7.3 million plus $1.7 million in EBRD grant funding to draw. Funded through every catalyst on this list.

What People are Missing

PhosCo trades at a fraction of its scoping study valuation. That study is about to be upgraded. The discount is identifiable: a tangled corporate history, marked by the project’s expropriation, a lapsed permit, and its eventual reissuance at a larger scale wholly to PhosCo, paired with a commodity most generalists do not understand, and the blanket Africa discount that Australian investors apply regardless of jurisdiction.

Every one of those factors is either resolved or resolving. Phosphate is now classified as a critical mineral by the US, Europe, and India, and sits on the UK’s watchlist of increasingly critical materials. Most of the world’s supply sources are either restricted, depleting, or disputed.

Tunisia is being de-risked by billions in multilateral investment. The macro tailwind is structural and the supply deficit does not have a quick fix. PhosCo holds 146 million tonnes of sovereign rock with EBRD backing, a scoping study update due in weeks, and cash to execute. Projects like Gasaat rarely stay under the radar for long.

This analysis is from The Drill Down, a daily briefing on critical minerals, junior mining, and capital markets. Join 2,200+ investors and operators who read it before the market opens. Subscribe HERE.

Disclosure: This article has been produced by Kamoa Capital, which provides advisory and investor relations services to mining companies. Kamoa Capital has a commercial relationship with PhosCo Ltd. The content is general in nature and does not constitute financial advice. Forward-looking statements, including those relating to the scoping study, are based on preliminary technical and economic assessments that are insufficient to support estimation of ore reserves. There is no certainty that the outcomes described will be achieved.