PGMs and Copper: Two Critical Minerals Deficits the West Cannot Close in Time

Platinum group metals are non-substitutable in the applications that matter. There is no replacement for platinum in PEM electrolysers. There is no replacement for palladium in catalytic converters at scale. There is no replacement for rhodium in petrol vehicle emissions control. The combined PGM market runs on supply that comes overwhelmingly from two countries, and one of them is Russia.

Copper has substitutes in some applications, aluminium replaces it in some transmission lines. Fibre optics in some communications cabling. But you cannot run an AI data centre on aluminium busbars and you cannot wind an EV motor with anything else. The world consumed roughly 28 million tonnes of refined copper in 2024 and S&P Global projects demand at 42 million tonnes by 2040, with supply peaking in 2030 and declining thereafter.

These are not parallel stories. They are the same story in different commodities.

The PGM supply concentration problem

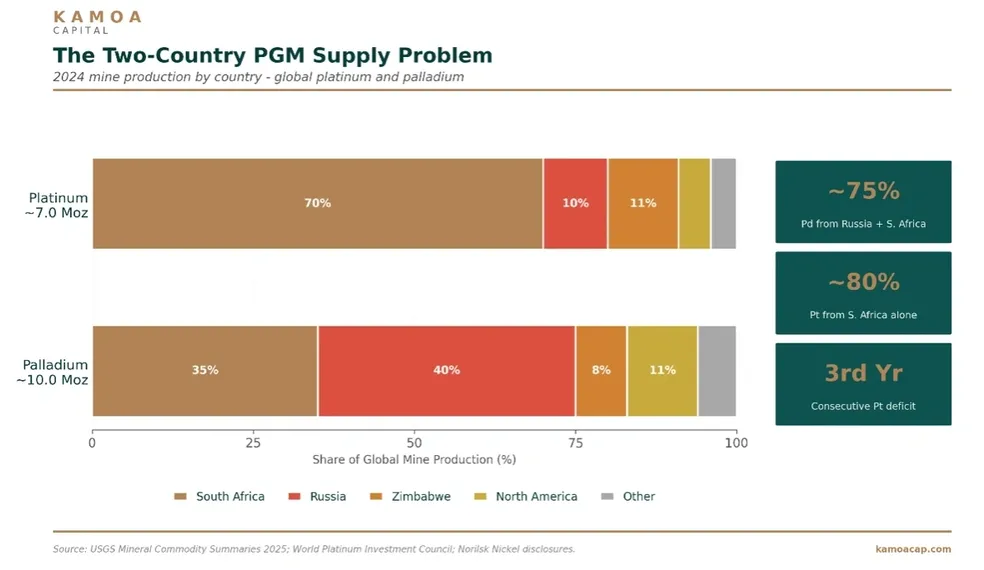

Roughly 70% of global platinum mine supply and 75% of global palladium supply comes from South Africa and Russia. South Africa is exhausted with mine grades falling, electricity supply from Eskom is unreliable, deep-shaft operating costs have risen sharply, and capital expenditure across the Bushveld has been contracting for a decade. Mined PGM output from South Africa fell around 5% year-on-year in the first ten months of 2025.

Russia is mid-sanctions and Norilsk Nickel reported its platinum output down 7% and palladium down 6% over the first nine months of 2025 due to equipment transitions and changes in ore composition.

Zimbabwe is the third producer with roughly 11% of global platinum, but it cannot scale. North America produces about 4 to 5% of platinum at Stillwater, the only US PGE operation, and Canada produces a small by-product stream.

The platinum market has been in deficit for three consecutive years. The World Platinum Investment Council estimated the 2025 shortfall at between 850,000 and 1.08 million ounces against total supply of around 7.2 million ounces. That is not a rounding error.

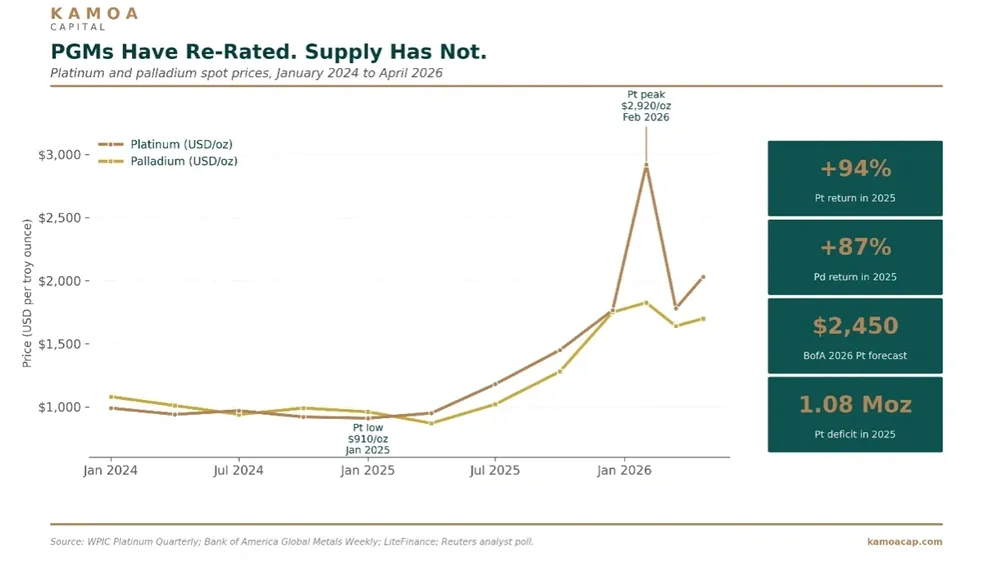

The price did what price does when supply is structurally short and demand is non-substitutable. Platinum traded at US$910 per ounce in January 2025. By mid-December 2025 it had reached US$1,766. By February 2026 it touched US$2,920 before consolidating around the US$2,000 level. Palladium tracked similar moves, gaining 87% over 2025. Rhodium ran from US$4,500 to US$7,500 per ounce.

Bank of America revised its 2026 platinum price forecast upward to US$2,450 per ounce, citing what it called “production discipline and inelastic mine supply.” In November 2025 the USGS added platinum, palladium and rhodium to the United States Critical Minerals List, with rhodium classified in the highest risk band.

Hydrogen is the demand vector being underestimated. WPIC expects hydrogen end-uses to account for 11% of total annual platinum demand by 2030, around 875,000 ounces. PEM electrolysers and heavy-duty fuel cell trucks are moving from pilot to deployment at the same time as PGM mine supply is shrinking. China reclassified platinum as a strategic critical mineral in late 2025 and imports more than 95% of what it consumes. Europe’s hydrogen targets are written into law.

This is the kind of analysis we publish daily in The Drill Down. Subscribe HERE for free.

The copper problem is the same problem in a different metal

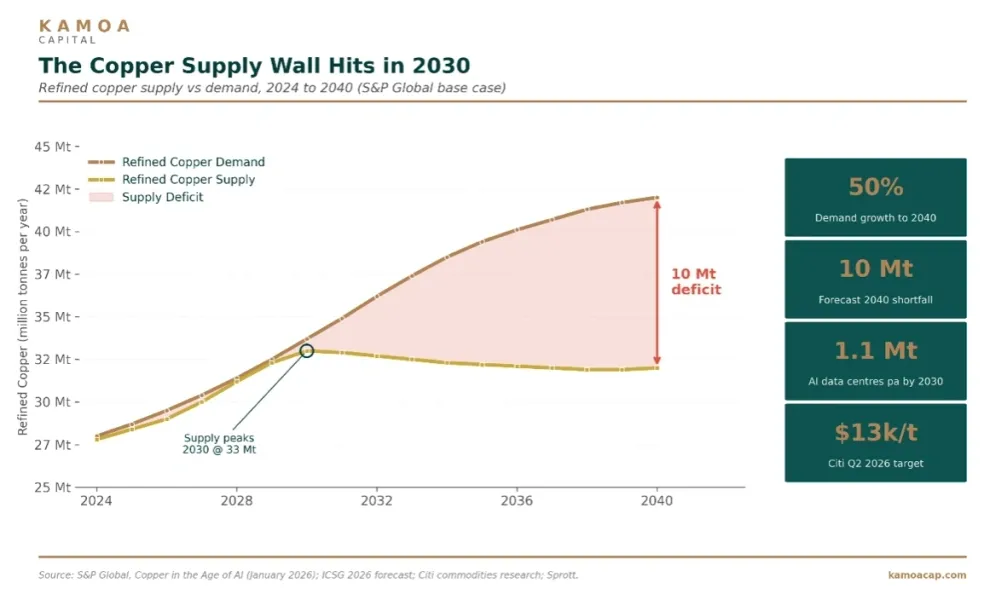

S&P Global published Copper in the Age of AI in January 2026. The headline number is a 10 million tonne supply deficit by 2040. Demand grows 50% to 42 million tonnes. Supply peaks at 33 million tonnes in 2030 and declines. Recycling more than doubles to 10 million tonnes and still does not close the gap.

The new demand layer is AI infrastructure. Sprott estimates data centres alone will consume 1.1 million tonnes of copper annually by 2030, around 3% of global demand. A single hyperscale facility takes up to 50,000 tonnes of copper. Anglo American cut its 2026 copper guidance in February. Kamoa-Kakula in the DRC and Grasberg in Indonesia have both delivered material 2025 disruptions. Citi has a Q2 2026 target of US$13,000 per tonne with a path to US$15,000 under disruption scenarios. Copper was added to the USGS Critical Minerals List for the first time in November 2025.

The copper response curve is the same as the PGM response curve. New mines take 15 to 20 years from discovery to first production in developed jurisdictions. The pipeline of copper projects that could come online before 2030 is largely already in development or further behind it. Anything that has not started construction by now will not contribute meaningfully to the 2030 supply equation.

GreenTech Metals: two deficits, one postcode

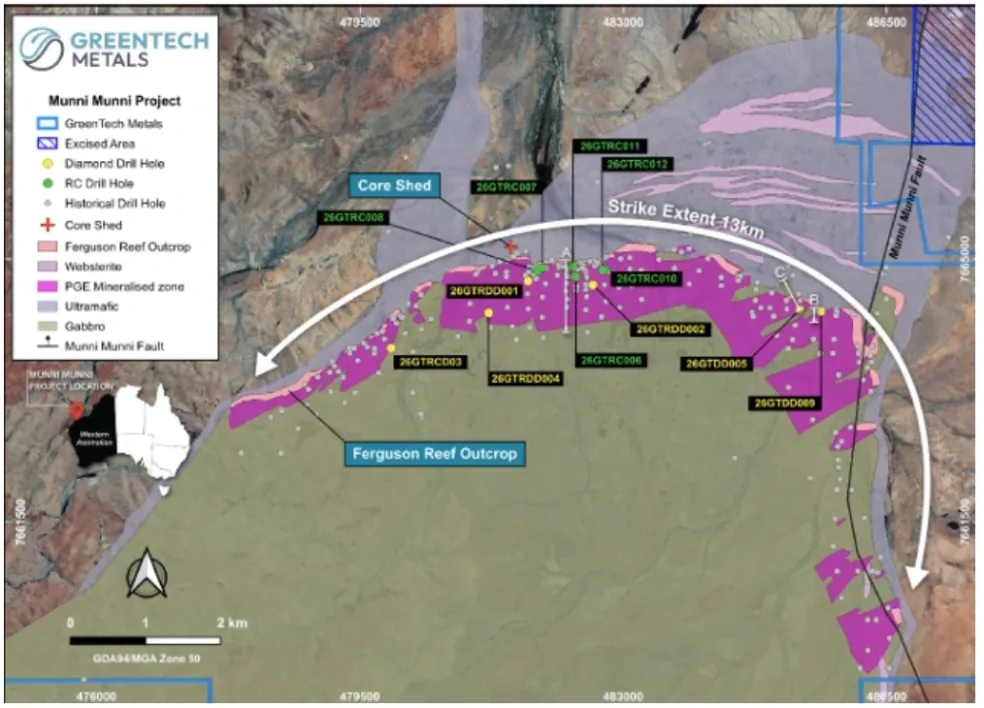

GreenTech Metals Ltd (ASX: GRE) is a roughly A$20 million market cap explorer in the West Pilbara of Western Australia. It has two contiguous projects covering both the PGM and copper deficit stories from the same address. The flagship is Munni Munni, a platinum-palladium-rhodium-gold-copper-nickel project acquired from Alien Metals (AIM: UFO) in February 2026. Adjacent and 100%-owned is Whundo, a high-grade brownfield VMS copper-zinc-gold project. The combined land package covers 346 square kilometres, including granted mining leases over the 33.5 square kilometre core of the Munni Munni intrusion.

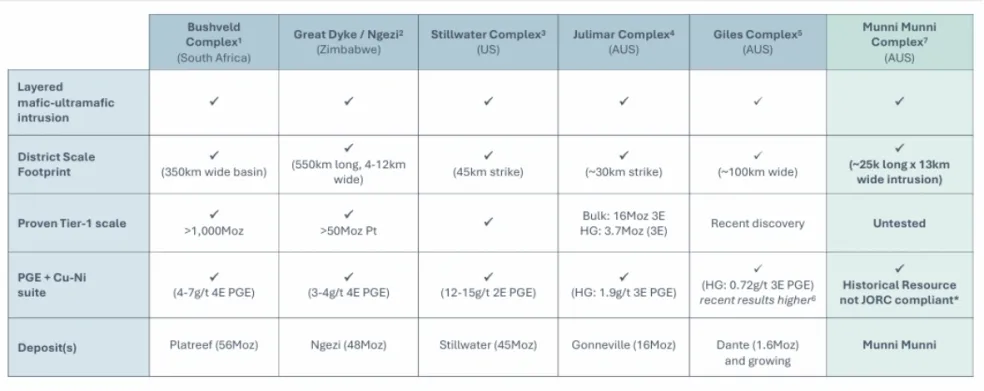

I have reviwed at most of the ASX-listed PGE explorers over the past 12 months. The set is small with most are single-asset stories chasing one thesis. Two things make GreenTech sit differently. First, Munni Munni is a layered mafic-ultramafic intrusion of the same family that hosts the Bushveld Complex, the Stillwater Complex, and the Great Dyke. The geology is well understood, the mineralised horizon named the Ferguson Reef has 90,000 metres of historical drilling across 396 holes behind it. Second, almost nobody is talking about Whundo, which sits next door with a proven copper resource and processing optionality already in place.

Munni Munni

The historical (JORC 2004) MRE is 24 million tonnes at 2.9 grams per tonne 4E for 2.2 million ounces. Broken out, that is 1,140,000 ounces of palladium, 830,000 ounces of platinum, 152,000 ounces of gold, and 76,000 ounces of rhodium. The historic resource also includes copper and nickel sulphide associated with the Ferguson Reef.

In December 2025 GreenTech raised A$5.2 million in an institutional placement at a meaningful premium to its prior trading range. Shareholders approved the acquisition in January 2026 and the deal completed in February. GreenTech now holds a 70% interest in Munni Munni with an option to go to 80%.

A Phase 1 drill program of 2,928 metres across 12 holes was completed ahead of schedule in March 2026, supplemented by resampling of 16 historical drill holes for a combined 2,199 samples now at ALS Global in Perth. Snowden Optiro is doing the QA/QC validation work to support a JORC 2012 Mineral Resource Estimate due in Q2 2026. Initial assays are expected very soon.

What matters is what GreenTech has already flagged from the historical dataset review and three things stand out for me.

- High-grade PGE zones grading above 4 grams per tonne PGE4 have been identified, well above the 2.9 grams per tonne reported average.

- Copper and nickel mineralisation extends beyond the Ferguson Reef boundaries and was not included in the 2004 estimate at all.

- Eastern zones of the deposit show a shallow plunge from surface, suggesting open-pit potential rather than the deep underground methods typically associated with reef-style PGE deposits.

A re-estimated JORC 2012 resource that incorporates higher grade tonnes, copper-nickel credits, and open-pit-amenable mineralisation is not what the market is currently pricing.

Whundo

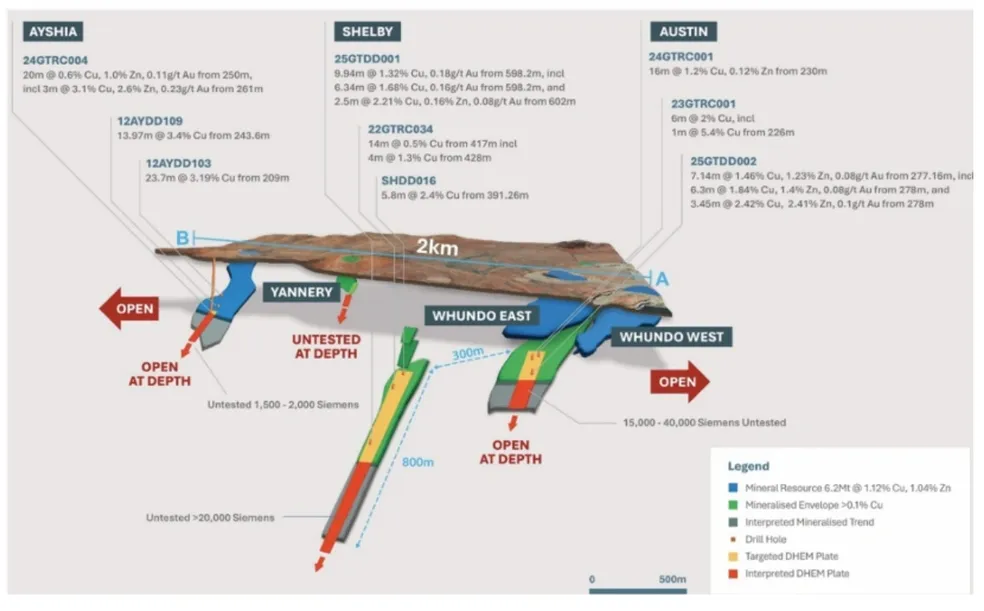

The Whundo Copper-Zinc-Gold Project is 100%-owned, sits 40 kilometres south of Karratha, and shares a boundary with the Munni Munni leases. It hosts a JORC 2012 Mineral Resource of 6.2 million tonnes at 1.12% Cu and 1.04% Zn for 45,000 tonnes of contained copper. That resource is built across just three of six known mineralised shoots: Whundo East, Whundo West, and Ayshia. The other three (Austin, Shelby, Yannery) are at advanced exploration stage and were not in the JORC count.

VMS deposits do not occur as single deposits rather they occur in clusters. Whundo has six confirmed shoots over a 2 kilometre strike, with a further 2 kilometres open in both directions. Recent diamond drilling at Austin and Shelby intersected high-grade copper sulphide mineralisation, including 7.14m at 1.46% Cu, 1.23% Zn at Austin and 9.94m at 1.32% Cu at Shelby. Downhole electromagnetic surveys identified additional conductor targets at depth.

The combined geophysical footprint of the Austin, Shelby and Yannery zones is approximately three times the size of the existing resource area.

Processing optionality is already in place. GreenTech had previously entered into an Alliance with Anax Metals (ASX: ANX) providing a pathway to treat Whundo ore through the fully-permitted Whim Creek processing hub. Artemis Resources’ Radio Hill plant sits 10 kilometres away. This is brownfield ore in tier-one Western Australia with processing infrastructure already in radius. Or with the copper and nickel potential at Munni Munni, the Whundo ore could feed into a consolidated GreenTech development plan.

The look through

What sits inside GreenTech today is the 2.2 million ounce Ferguson Reef historical resource, plus what the company has flagged in its own April 2026 announcement that is not in that number. High-grade PGE zones above 4 g/t PGE4 identified in the historical data review. Copper and nickel sulphide mineralisation outside the Reef horizon. Shallow eastern zones at 30-degree plunge with open-pit geometry. Eight kilometres of strike continuing under Fortescue Basin cover that has never been drilled. The 100%-owned Whundo 6.2 million tonne copper-zinc-gold resource on the adjoining tenure with a 15 to 23 Mt exploration target and a Whundo MRE update including gold credits guided for H2 2026. The Andover Lithium joint venture with Artemis Resources holding 420 km² of the West Pilbara lithium corridor.

A re-statement of the Ferguson Reef to JORC 2012 standard, incorporating copper and nickel credits and open pit amenable eastern zone material, is a different reporting basis to the historical estimate.

GreenTech trades at approximately A$20 million, with 274.5 million shares on issue and A$2.4 million in cash at 31 March 2026.

Catalysts

- Initial Phase 1 drilling assays from Munni Munni, expected very soon

- JORC 2012 Mineral Resource Estimate at Munni Munni, expected Q2 2026

- Re-statement to include copper and nickel credits outside the Ferguson Reef

- Open-pit scoping work on the shallow eastern zones

- Whundo resource extension drilling and DHEM follow-up at Austin, Shelby, Yannery, Ayshia

What people are missing

Two commodity deficits cannot be closed inside a single decade. South African PGM mines are not getting deeper or cheaper. Russian export reliability is not improving. China is not reducing its dependence on imported platinum. Copper supply growth out to 2030 was effectively locked in five to ten years ago by what was approved for development then. Almost nothing in the current pipeline arrives in time.

Sitting in tier-one Western Australia, on granted mining leases, with a 2.2 million ounce historical PGM resource about to be re-stated under JORC 2012, an adjacent VMS copper-zinc system with processing infrastructure in radius, a real institutional register, the asymmetry deserves a look.

Sources

USGS Mineral Commodity Summaries 2025; USGS Final 2025 List of Critical Minerals (Federal Register, 7 November 2025); World Platinum Investment Council Platinum Quarterly Q4 2025 and January 2026 Five-Year Outlook; Bank of America Global Metals Weekly, 9 January 2026; S&P Global, Copper in the Age of AI: The Challenges of Electrification, 8 January 2026; International Copper Study Group 2026 forecast; Citi, JP Morgan, Goldman Sachs 2026 copper price forecasts; Sprott Asset Management PGM commentary October 2025; Chalice Mining (ASX: CHN) Gonneville PFS announcement, 8 December 2025; GreenTech Metals (ASX: GRE) ASX announcements December 2025 through April 2026; Alien Metals (AIM: UFO) RNS announcements covering Munni Munni JV; Hoatson and Keays (1989), Economic Geology, 84(7); Hoatson and Sun (2002), Economic Geology, 97(4).

This analysis is from The Drill Down, a daily briefing on critical minerals, junior mining, and capital markets. Join 2,900+ investors and operators who read it before the market opens. Subscribe HERE.

Disclosure

Kamoa Capital has a commercial relationship with GreenTech Metals Ltd. This article is general in nature and does not constitute personal financial advice. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. This article contains forward-looking statements based on current expectations and assumptions that are subject to risks and uncertainties. The historical Mineral Resource Estimate at Munni Munni referenced is a JORC (2004) estimate and is not reported in accordance with the JORC Code (2012). Past performance is not a reliable indicator of future performance.